A Basic Assumption Used in Most Economic Theories Is That

Theory of Consumer Demand. All economic theories have been developed on the assumption of a capitalist economy in which the means of production and distribution are privately owned and used for personal gain.

2

The role of an assumption in an economic theory is to.

. Restrict the analysis to the effect of a single economic factor. It is in this second sense that theory will be used in this paper. A as price goes up the amount purchased will go up too.

Equilibrium is another basic assumption of Economics. A basic assumption used in most economic theories is that. As price decreases quantity demanded will increase.

All other things remain the same. The economy is assumed to be in equilibrium markets are efficient and perfect. The main ones are that people have rational preferences they are self-interested they are utility maximisers and they have access to all relevant information including information about the future.

Market forces decide most economic questions. Question 10 5 5 pts A basic assumption used in most economic theories is that. Accordingly an economic theory eg the neoclassical theory of con-sumer choice is a set of statements organized in a characteristic way and designed to serve as partial premisses for explaining as well as predicting an indeterminately large and usually varied class of eco-.

But when we decide on one particular thing we are. A basic assumption used in many economic models is. Every firm or a consumer will try to reach the equilibriumThe producer gets equilibrium when he gets maximum profits.

B as price goes up less will be offered for sale on the market. The most important and key assumption of Economics is that all the people and organizations are intelligent have all the information and therefore they all will work in a rational way. Assumptions in Microeconomic Theory.

Whatever goes up must come down. As price decreases quantity demanded will increase. It assumes stable government and certain socio-economic institutions which include private property self-interest economic liberalism or laissez-faire competition and the price system.

And as a result its impossible to satisfy each of our wants making it a necessity for us to make choices. Basic Assumptions in Economics People are Rational. People act independently on the basis of full and relevant information.

We suppose that there is equilibrium. Make things easier by avoiding normative issues. A a theory is a guess or hunch about something that has occurred in nature B a theory is based on verifiable laws that can be proven true C a theory is a set of ideas that explains a.

C if the underlying theory doesnt represent reality it is not useful. What is true for a part of the whole must also be true for the whole. Theory of Production Input Value.

There are various economic theories to help explain how an economy. Summery and Conclusion Neo-classical economics works with three basic assumptions. Similarly consumer gets equilibrium when he gets maximum satisfaction.

Raw materials components goods and other supplies are limited. Scarcity or paucity refers to limitation. The assumptions of economists are made to better understand consumer and business behavior when making economic decisions.

Neo-classical economics works with three basic assumptions. People have rational preferences among outcomes that can be identified and associated with a value. Theory of Opportunity Cost.

According to economists there are five basic assumptions that we make regarding economics. The standard or neo-classical view of economics makes a lot of assumptions. D ceteris paribus which means all other things remain unchanged.

Individuals make most economic choices. Make the complexities of the real world more abstract to focus more sharply upon the issues under examination. Facilitate the economists job of obscuring simple relationships behind economic variables.

There are two key assumptions used in the economic theory of firms you should review before looking at pricing and output decision-making in the four types of markets. Therefore the chance of a theory going wrong by relying on these assumptions is very rare. Economists assume that humans have limitless wants where scarcity exists.

An economic theory uses assumptions to A. Almost all of the models studied in traditional economics courses begin with an assumption about the rationality of the parties involved rational consumers rational firms and so on. Individuals maximize utility as consumers and firms maximize profit as producers.

When we usually hear the word rational we tend to interpret it generally as makes well. People act independently on the basis of full and relevant information. The Rationality Assumption in Neoclassical Economics.

Individuals maximize utility as consumers and firms maximize profit as producers. People have rational preferences among outcomes that can be identified and associated with a value. What is true for a part of the whole must also be true for the whole.

2

Pin By Learncbse Ncert Solutions On Ap Economics In 2021 Economics Notes Micro Economics Economics Lessons

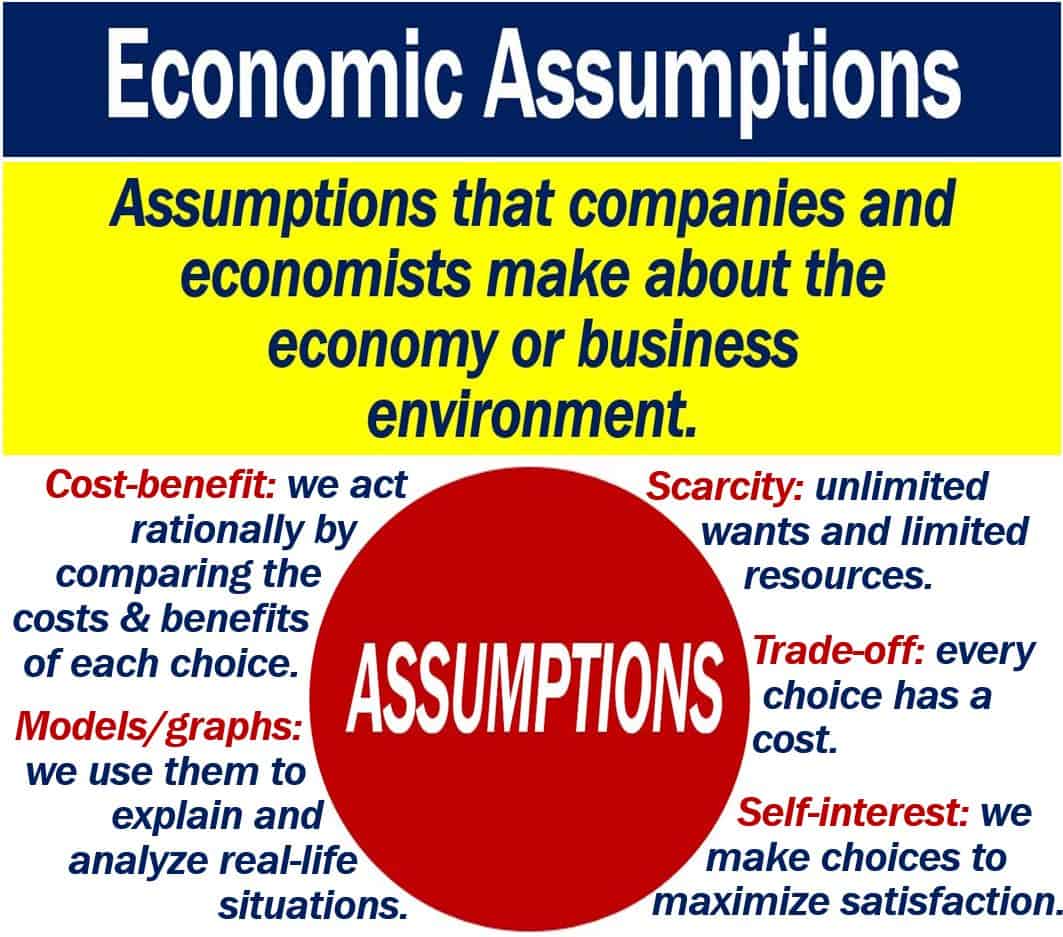

What Are Economic Assumptions Definition And Examples Market Business News

2

2

2

Study Suggests A Key Assumption Of Economic Oxford Martin School

We Have Mind Mapped For You Thinking Fast And Slow By Daniel Kahneman Key Takeaways One Sentence Summary A Thinking Fast And Slow Mind Map Fast And Slow

/laissez-faire-definition-4159781-V2-828107953ee443f1bdeaaaba9b35759b.jpg)

What Is Laissez Faire Economic Theory

2

2

Modigliani Miller Theory On Dividend Policy Accounting And Finance Accounting Education Dividend

2

2

2

2

/GettyImages-1251235330-83979ee0c47441b284d9c4eecee5a72f.jpg)

Economists Assumptions In Their Economic Models

Hypotheses Favoring Profit Maximization Profit Hypothesis Theories

Theoretical Economics Letters

Comments

Post a Comment